Why would a growing enterprise continue to sacrifice 3% of every high-value invoice to credit card fees when a more strategic path exists? You likely recognize the friction caused by slow paper check clearing and the persistent risk of manual data entry errors in your QuickBooks workflows. It’s a common challenge for leaders who want to maintain a steady cash flow without the heavy tax of traditional processing. By adopting electronic check processing for business, you can reclaim those margins and move away from the logistical hurdles of the past.

We’re here to act as a steady hand through this transition toward a more resilient financial infrastructure. This guide shows you how to leverage modern payment rails to reduce costs and automate your reconciliation processes. We’ll examine the impact of the June 2026 Nacha fraud monitoring rules and show you how to integrate these tools with your current accounting systems for a seamless experience. You’ll gain a clear roadmap for faster access to funds and a more transparent, professional approach to managing your B2B treasury needs.

Key Takeaways

- Analyze the fiscal advantages of flat-fee structures against percentage-based interchange to understand why eChecks are a more strategic choice for high-value B2B invoices.

- Identify the differences between digital signatures and recorded verbal consent to ensure your 2026 authorization protocols meet the highest security standards.

- Streamline your accounting workflows by implementing electronic check processing for business through direct QuickBooks integration for automated, real-time reconciliation.

- Evaluate merchant service providers based on their ability to handle high-volume demands and their specialized knowledge of the Milwaukee corporate environment.

- Master the modern B2B payment lifecycle to ensure faster access to funds while maintaining full compliance with the latest Nacha fraud monitoring requirements.

What is Electronic Check Processing for Business?

Electronic check processing for business is the digital evolution of the traditional paper check, utilizing the Automated Clearing House (ACH) network to move funds between corporate bank accounts. While the experience for your client feels familiar, the underlying technology is far more sophisticated than a simple scan of a physical document. In 2026, this process has matured into a highly secure, data-rich transaction method that adheres to rigorous encryption standards and real-time verification protocols. By understanding what an electronic check is, leaders can see how it serves as a bridge between legacy accounting habits and the speed of modern B2B commerce.

The transition away from physical check lockboxes is a strategic move for most Milwaukee firms. Maintaining a lockbox requires manual labor, physical transport, and significant bank fees that eat into your margins. As corporate entities prioritize efficiency, they’re migrating toward digital solutions that eliminate the multi-day delay inherent in postal delivery and manual sorting. This shift is governed by Nacha, the organization that manages the ACH network. Nacha’s 2026 standards ensure that every business-to-business transfer includes the necessary metadata for fraud prevention and accurate record-keeping, providing a level of security that paper checks simply can’t match.

How eChecks Differ from Traditional ACH

It’s helpful to view the ACH network as the engine and the eCheck as the specialized vehicle designed for business payments. While all eChecks are ACH transactions, not all ACH transfers are eChecks. The term “eCheck” refers to the specific user interface and authorization process that mimics the workflow of a check, making it easier for your clients to adopt. For a corporate treasurer, an eCheck represents the digital authorization layer that converts a standard payment request into a structured ACH transaction; this maintains a clear audit trail without the latency of physical handling. This distinction allows businesses to enjoy the low cost of the ACH network while using a format that fits naturally into existing accounts receivable processes.

The Business Case for Digital Check Adoption

Adopting electronic check processing for business provides immediate relief from the “check is in the mail” uncertainty that plagues B2B cash flow. Digital tracking allows your finance team to see exactly when a payment was initiated, authorized, and cleared. This visibility reduces the administrative burden of chasing late invoices and improves your ability to forecast capital needs. Beyond the financial benefits, the move to paperless workflows offers several operational advantages:

- Reduced Overhead: You’ll eliminate the need for physical storage, courier services, and manual bank deposit trips.

- Enhanced Security: Digital transactions are encrypted and monitored by 2026 fraud-detection AI, unlike paper checks which are vulnerable to interception and forgery.

- Sustainability: Removing paper and physical transport from your payment cycle significantly lowers the environmental footprint of your back-office operations.

If you’re currently managing high-volume invoices, the reduction in manual data entry alone can save your team dozens of hours each month. It’s a transition that doesn’t just save money; it protects your time and strengthens your professional reputation with vendors who value prompt, reliable payments.

The Mechanics of High-Volume B2B eCheck Transactions

Managing thousands of monthly corporate payments requires more than just a digital interface; it demands a systematic approach to batching and data integrity. In 2026, the lifecycle of a high-volume B2B transaction begins with a multi-layered authorization. Unlike consumer payments, enterprise-grade electronic check processing for business utilizes sophisticated batching engines. These systems aggregate large volumes of invoices throughout the day, submitting them to the ACH network in structured files that minimize processing overhead and ensure consistent delivery. Understanding how electronic check processing works at this scale reveals a workflow designed for maximum efficiency and auditability. For firms scaling their transaction volumes, mastering high volume ACH processing is an essential step toward building a resilient and cost-effective payment infrastructure.

Authorization protocols have become more stringent to align with the Nacha fraud monitoring rules implemented in June 2026. While digital signatures are the primary standard for high-ticket B2B transactions, some workflows still utilize recorded verbal consent for specific service-based agreements. Regardless of the method, the data must be captured and stored securely to meet compliance standards. Once authorized, the transaction enters a clearing cycle where it’s verified against the payer’s account before settlement. This methodical progression ensures that funds are moved with a high degree of finality, providing the stability required for large-scale treasury management.

Security Protocols for Corporate Transfers

Security is the foundation of modern B2B payments. In 2026, industry standards mandate AES-256 encryption for all data at rest and in transit. Tokenization is also a critical component; it replaces sensitive bank account details with unique digital identifiers, ensuring that a breach of your local accounting system doesn’t expose your clients’ financial data. Our team focuses on providing high volume merchant services that incorporate advanced identity verification and account validation tools. These systems cross-reference transaction data against known fraud databases in real time, significantly reducing the risk of unauthorized returns or administrative errors for Milwaukee-based firms.

Understanding Settlement Cycles

Settlement timelines are a vital consideration for managing corporate cash flow. While standard ACH processing typically settles within two to three business days, many enterprise-grade accounts now opt for Next-Day ACH settlement to bridge the gap between payment and liquidity. The current banking landscape also offers integration with real-time payment rails for immediate finality when needed. Factors such as the timing of your batch submission and the specific risk profile of the transaction can influence these windows. By aligning your accounts receivable workflows with these cycles, you can maintain a predictable and healthy cash position without the delays associated with traditional paper check clearing.

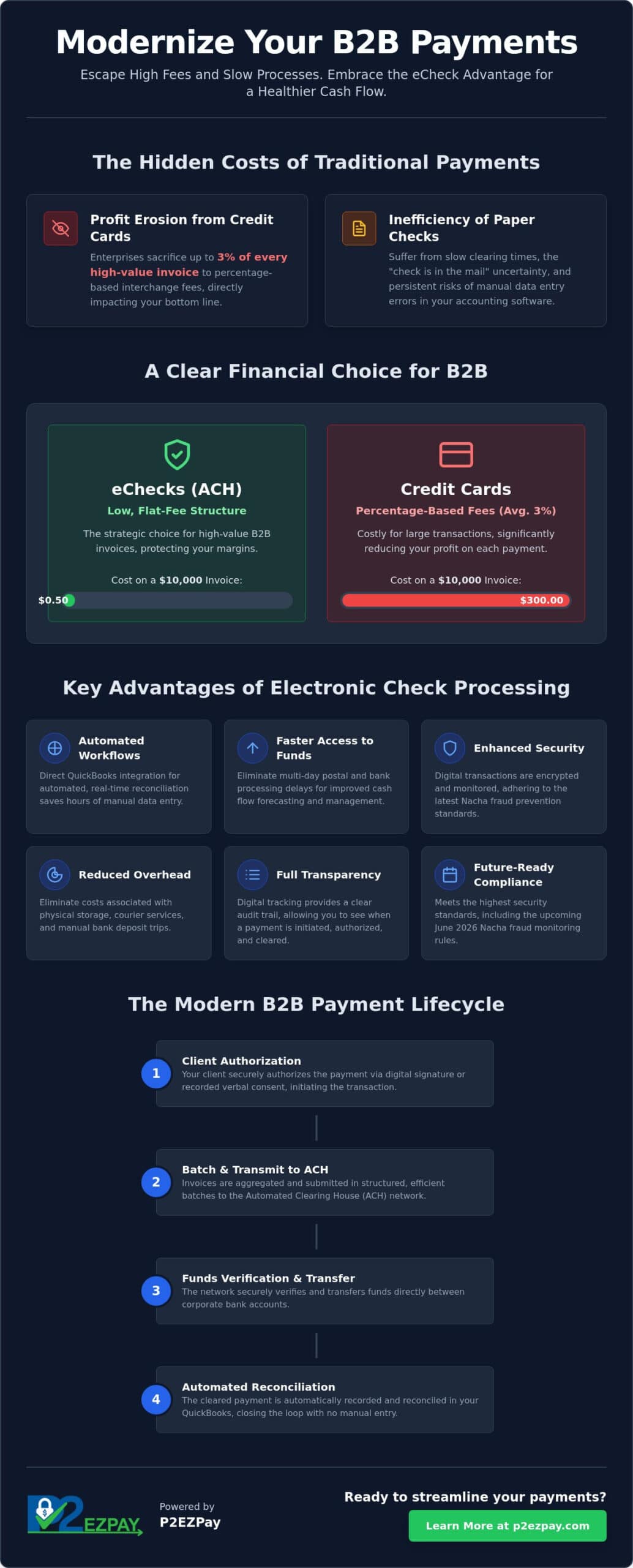

eChecks vs. Credit Cards: A Cost-Benefit Analysis

Choosing between payment methods isn’t just about convenience; it’s a strategic decision that directly affects your bottom line. Credit card transactions operate on a percentage-based interchange model, which can quickly become prohibitive as invoice totals rise. If you process a $50,000 shipment at a 2.5% fee, your business loses $1,250 just to accept that single payment. In contrast, electronic check processing for business typically relies on flat-fee structures. This means your cost remains consistent whether the invoice is for $500 or $50,000, allowing you to retain a much larger portion of your revenue and maintain healthier margins.

You should also consider the difference in dispute rights and payment finality. Credit cardholders enjoy extensive chargeback protections under federal regulations, which can lead to administrative headaches or “friendly fraud” disputes. Bank-to-bank transfers via the ACH network have more stringent requirements for B2B disputes, especially after the 2026 Nacha updates. This provides your firm with greater security and reduces the likelihood of unexpected reversals long after the goods have been delivered. While offering both options is often necessary to maintain strong client relationships, steering high-ticket partners toward eChecks is a wise move for your treasury’s stability.

Interchange Optimization and Level 3 Data

If your clients insist on using corporate cards, you can utilize Level 2 and Level 3 data to lower your interchange rates. These protocols require providing detailed transaction information, such as purchase order numbers and line-item details, to qualify for lower processing tiers. While this optimization is valuable for managing card-heavy portfolios, eChecks allow you to bypass these complex commercial card tiers entirely. Transitioning just one $10,000 invoice from a corporate card to an eCheck can save your business over $250 in fees, which represents a significant return on investment for a simple change in payment workflow.

Operational Efficiency Comparison

Managing high-volume payments requires a focus on reconciliation and failure handling. Credit card failures usually happen at the point of sale, whereas eCheck failures, such as Non-Sufficient Funds (NSF) notifications, typically arrive during the clearing window. However, modern systems now provide automated alerts and specific return codes that simplify the re-collection process. For growing Milwaukee distribution firms, the scalability of electronic check processing for business is unmatched. As your volume increases, your processing costs don’t rise linearly, providing a stable foundation for long-term expansion and more predictable cash flow management. To understand how to build the infrastructure needed to support this growth, review our comprehensive high volume ACH processing strategy guide for scalable B2B payments.

Integrating eChecks with QuickBooks and Financial Workflows

For many Milwaukee firms, the true value of electronic check processing for business isn’t found just in lower fees; it’s found in the hours of administrative labor reclaimed through automation. Manual data entry remains one of the most significant sources of error in accounts receivable. When your payment gateway operates in a silo, your team is forced to move data between systems, increasing the risk of misapplied payments or double-entry mistakes. A seamless connection between your merchant services and your ledger provides a single source of truth, ensuring that every B2B transaction is reflected accurately and immediately.

Our approach to QuickBooks payment integration focuses on removing these technical obstacles. By facilitating a direct link between the ACH network and your accounting software, P2EZPay allows payments to be initiated and recorded in one step. This integration gives you real-time visibility into your cash flow, allowing you to see which B2B invoices are pending and which have settled without waiting for a manual end-of-day report. This clarity is vital for treasurers who need to make agile decisions regarding capital allocation and vendor payments. For a deeper look at automating these workflows and staying ahead of 2026 NACHA compliance requirements, explore our comprehensive guide to QuickBooks ACH integration for B2B payment automation.

Step-by-Step QuickBooks Integration Guide

Connecting your financial workflows doesn’t have to be a complex engineering project. Whether you utilize QuickBooks Online for its accessibility or QuickBooks Desktop for its robust reporting, the integration process follows a logical path to ensure data integrity:

- Merchant Account Linkage: You’ll begin by securely connecting your eCheck processing account to your specific QuickBooks company file using encrypted API credentials.

- Automated Posting: Configure the system to automatically mark invoices as “Paid” once the eCheck authorization is received, eliminating the need for manual status updates.

- Sync Verification: Establish a routine for verifying sync accuracy during the first few billing cycles to ensure that all transaction metadata, such as invoice numbers and customer IDs, is mapping correctly.

Automating the Reconciliation Process

The final hurdle in many financial workflows is the reconciliation of bank deposits against ledger entries. In an integrated environment, this process becomes largely invisible. The software automatically matches the lump-sum deposits in your bank feed to the individual eCheck transactions recorded in QuickBooks. If an exception occurs, such as a return for non-sufficient funds, the system can automatically reverse the payment and notify your team to take action. This level of automation allows Milwaukee firms to scale their transaction volume significantly without the need to add additional headcount to the accounting department. It’s a strategic way to build a leaner, more responsive financial operation that supports long-term growth.

Choosing a B2B Merchant Service Partner in Milwaukee

Selecting a payment partner is a long-term commitment that directly influences your firm’s operational agility. For Wisconsin-based corporate entities, local expertise is more than just a convenience; it’s a strategic asset. Milwaukee’s industrial and distribution hub requires a partner who understands the specific pressures of high-volume logistics and the necessity for reliable electronic check processing for business. A local provider offers a level of accountability that national, faceless processors can’t match, ensuring your treasury operations remain stable and responsive to the regional market’s demands.

As we look toward the complexities of 2026, evaluating high-volume merchant account providers requires a focus on strategic alignment rather than just transaction rates. You need a partner that acts as a seasoned mentor, guiding you through the nuances of Nacha compliance and evolving security standards. The P2EZPay approach is grounded in a deep commitment to your success, acting as a steady hand as you navigate the technical nuances of the modern financial sector. This partnership ensures that your infrastructure is built for growth, allowing you to adapt to new payment rails while maintaining the cost-efficiency of your established workflows.

Local Support vs. National Call Centers

When a high-value batch transaction encounters a technical hurdle, waiting in a national call center queue isn’t a viable option for a busy treasurer. A Milwaukee-based partner provides direct access to personalized account management, where the person handling your inquiry understands your business’s history and local market context. This proximity allows for faster troubleshooting and a more nuanced approach to service delivery. It’s the difference between being a ticket number in a global database and having a loyal ally who is deeply invested in your firm’s success.

Customizing Your Payment Suite

Every industry has unique cash flow rhythms. A wholesale distributor in the Menomonee Valley has different requirements than a professional services firm in Downtown Milwaukee. Your payment suite should reflect these differences, combining Ecommerce Payment Processing with robust back-office tools for electronic check processing for business. By tailoring your ACH and eCheck solutions, you can create a bespoke environment that mirrors your existing workflows rather than forcing your team to adapt to a generic model. To begin this transition, you can request a professional payment audit from P2EZPay to identify specific areas for cost reduction and automation.

Optimizing your corporate payment infrastructure is the final step in securing your firm’s financial future. Whether you’re seeking better integration for your high-ticket invoices or a more transparent fee structure, the right partner makes the transition seamless. It’s about removing obstacles and fostering a sense of confidence in every transaction you process. By choosing a partner who values wisdom and community as much as technical proficiency, you’re investing in a relationship that grows alongside your business.

Securing Your B2B Treasury Strategy for 2026 and Beyond

Modernizing your payment infrastructure is about more than digital convenience; it’s a strategic move to protect your margins and streamline your back office. By shifting high-value invoices to electronic check processing for business, you replace unpredictable percentage-based fees with a stable, flat-cost model. This transition doesn’t just save capital. It also reduces the administrative friction of manual reconciliation through automated, real-time accounting synchronization. Your finance team can finally move away from the uncertainty of paper checks and the high cost of corporate cards.

As we navigate the complexities of 2026 fraud rules and real-time settlement windows, having a seasoned mentor makes all the difference. Our team brings over 30 years of industry experience and specialized QuickBooks integration support to every partnership. We’re proud of our local Milwaukee presence, offering the hands-on guidance required to build a resilient payment suite tailored to your unique industry needs. We’re here to act as a steady hand, ensuring your financial operations are both secure and highly efficient.

Schedule a consultation with our Milwaukee-based B2B experts to conduct a professional audit of your current payment workflows. We’re ready to help you build a more efficient, secure, and profitable future for your firm.

Frequently Asked Questions

Is electronic check processing safe for high-value B2B transactions?

Yes, it’s exceptionally safe for large scale transfers because it utilizes the latest AES-256 encryption and tokenization. The 2026 Nacha fraud monitoring rules also require originators to maintain risk-based monitoring, providing a robust layer of protection that paper checks lack. These protocols ensure that sensitive bank details are never exposed during the transfer process.

How long does it take for an eCheck to clear in 2026?

Most transactions clear within two to three business days, though Next-Day ACH settlement is now a standard option for many enterprise accounts. The actual clearing time depends on your specific batch submission deadlines and the risk profile of the transaction. Some modern processors also integrate with real-time payment networks to provide even faster finality when your cash flow requires it.

What is the difference between ACH and an eCheck?

An eCheck is a specific type of transaction that uses the ACH network as its underlying rail. You can think of the ACH network as the nationwide infrastructure for moving money and the eCheck as the digital “vehicle” that carries the payment instructions. For a business, the term eCheck usually refers to the user-facing interface that mimics a traditional check workflow.

Can I integrate eCheck payments directly into QuickBooks?

Yes, you can integrate these payments directly into both QuickBooks Online and Desktop versions. This connection allows your system to automatically mark invoices as paid and match deposits to your bank feed. It’s a vital feature for Milwaukee firms that want to eliminate manual data entry and maintain a single source of truth for their financial records.

What are the typical fees for electronic check processing for business?

Fees are generally structured as flat per-transaction charges rather than the percentage-based interchange seen with credit cards. This makes electronic check processing for business a more cost-effective choice for large invoices where a 3% fee would be prohibitive. By using a flat-fee model, your processing costs remain predictable regardless of the total dollar amount on the invoice.

How do I handle a bounced eCheck or NSF notification?

Your payment gateway will provide an automated notification with a specific return code, such as R01 for insufficient funds, as soon as the bank reports the failure. You can then use your integrated accounting tools to automatically reverse the payment in your ledger and notify the client. Many systems also allow you to re-initiate the transaction after a set period to recover the funds without manual intervention.

Do eChecks require special hardware or POS terminals?

No, you don’t need any physical hardware or specialized POS terminals to accept digital checks. All transactions are handled through a secure virtual terminal or directly within your integrated accounting software. This lack of hardware requirements makes it an ideal solution for remote sales teams and back-office accounting departments that handle high volumes of B2B invoices.

Can I accept eChecks for recurring B2B service contracts?

Yes, they’re an excellent choice for recurring billing such as monthly retainers or long-term service agreements. Once your client provides a one-time authorization, you can schedule the system to pull funds automatically on a set date each month. This ensures your business receives payments on time without requiring the client to manually initiate a transfer for every billing cycle.