Most B2B organizations treat their payment systems as a simple utility, but in 2026, an unoptimized infrastructure is actually a silent drain on your bottom line. You likely feel the friction every time your team spends hours on manual data entry in QuickBooks or when high interchange fees eat into your margins on large credit card transactions. It’s frustrating to watch slow reconciliation of ACH and e-check payments stall your cash flow while you wait for funds to clear. Relying on outdated corporate electronic payment services shouldn’t be the cost of doing business; it’s a hurdle that prevents your financial department from reaching its full potential.

We’ve designed this guide to help you move beyond basic tax compliance and toward a high-performance payment strategy that works for you. You’ll discover how to implement automated financial workflows that eliminate human error and leverage Level 2 and Level 3 processing to secure significantly lower transaction costs. We will walk through the latest 2026 regulatory updates, including Nacha’s new fraud monitoring requirements, and show you how local, Milwaukee-area support can transform your B2B operations into a streamlined engine for growth.

Key Takeaways

- Modernize your approach to corporate electronic payment services by transitioning from manual bank wires to integrated B2B solutions that support strategic growth.

- Conduct a detailed cost-benefit analysis of ACH and e-check services to determine the most efficient processing methods for high-volume corporate environments.

- Resolve the “Automation Gap” by synchronizing payment data directly into QuickBooks, allowing for real-time financial reporting and the elimination of manual data entry.

- Leverage specialized Level 2 and Level 3 processing techniques to capture lower interchange fees on B2B credit card transactions.

- Identify the specific criteria for selecting a high-volume merchant partner in Wisconsin who provides the local expertise and mentorship your business requires.

Understanding Corporate Electronic Payment Services in 2026

Many executives still view their payment infrastructure through the narrow lens of compliance, often associating it primarily with tax deadlines and government portals. However, in 2026, high-performance corporate electronic payment services have evolved far beyond mere tax filings. The modern B2B landscape is shifting away from manual bank wires, which are prone to human error and lack transparency, toward integrated merchant solutions. These systems don’t just move money; they embed financial logic directly into your daily operations.

Corporations are increasingly prioritizing “invisible payments” within their tech stacks. This means that financial transactions occur as a background process within your existing software, triggered by events like a signed contract or a fulfilled order. This automation relies on a sophisticated electronic funds transfer (EFT) framework that ensures speed and security without requiring a manual click for every invoice. When you explore B2B payment processing solutions, you’ll see that the goal is to make the movement of capital as seamless as the data that travels with it.

Commercial vs. Regulatory Payment Portals

It’s a common mistake to assume that because your team uses IRS Direct Pay or state portals, your payment needs are covered. These regulatory tools are designed for one-way compliance, not for the complex, two-way nature of vendor management or payroll. Consumer-grade bank transfers often lack the data attachments necessary for automated reconciliation, leaving your accounting team to piece together why a specific payment was made. Without a robust commercial infrastructure, your business remains tethered to manual oversight that slows down growth.

The Role of Merchant Service Advisors

Choosing the right setup isn’t about downloading an app; it’s about strategic alignment. A professional merchant services advisor acts as a mentor, helping you navigate the nuances of Level 2 and Level 3 data requirements to lower your overhead. Unlike “off-the-shelf” software that offers a generic experience, a consultancy-led approach ensures your payment architecture is built for the specific volume and complexity of your business. This partnership provides the steady hand needed to protect your margins while scaling your operations.

High-Volume B2B Infrastructure: ACH and E-Checks

Managing high-volume transactions requires a shift from convenience-focused processing to cost-efficient infrastructure. While credit cards offer speed, the interchange fees on a six-figure B2B invoice can be staggering. This is where ACH and e-check solutions become the backbone of corporate electronic payment services. Unlike card networks, ACH often operates on a flat-fee or significantly lower percentage basis, saving your organization thousands in annual overhead. It’s about choosing the right tool for the scale of the task.

Scaling these operations isn’t just about handling more transactions; it’s about maintaining integrity under pressure. Robust systems, similar to the high-capacity infrastructure used by Pay.gov, ensure that volume doesn’t compromise speed or security. If your business is expanding, you’ll need a High volume ACH processing strategy that accounts for the 2026 Nacha fraud monitoring mandates. These rules, effective in phases throughout 2026, require non-consumer originators to implement enhanced monitoring to combat sophisticated fraud schemes.

Why E-Checks are Essential for Corporate AR

Collecting on high-ticket invoices shouldn’t feel like a hurdle for your clients. By implementing electronic check processing for business, you provide a familiar, secure method for vendors to pay without the limitations of credit card caps. This reduces friction in your accounts receivable cycle and ensures that funds move directly from bank to bank, often clearing much faster than traditional paper checks. It’s a professional way to respect your client’s cash flow while protecting your own.

Managing High-Volume Transaction Risks

Security in a corporate environment is non-negotiable. As volume increases, so does the risk of “false pretenses” fraud, such as vendor impersonation or payroll diversion. We utilize advanced encryption and PCI-compliant protocols to protect every transfer within your ecosystem. To ensure your business remains protected against evolving threats, it’s wise to consult with a payment specialist who understands the specific risks of the Wisconsin corporate market.

Maximizing Efficiency with QuickBooks Payment Integration

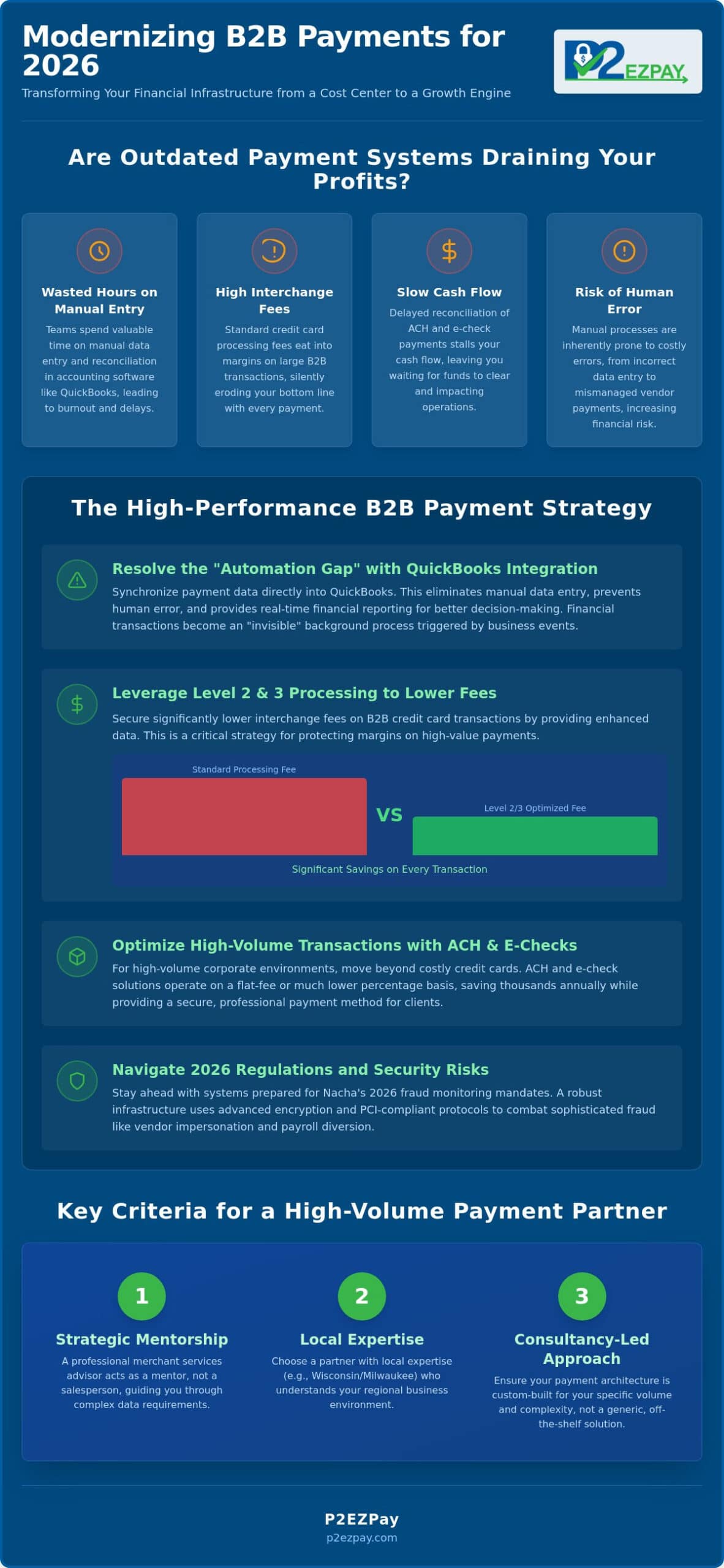

The “Automation Gap” remains one of the most significant hidden costs in modern accounting. When your team manually matches bank statements to invoices, they aren’t just performing a task; they’re draining resources that could be used for strategic analysis. High-performance corporate electronic payment services bridge this gap by synchronizing payment data directly into your ledger in real-time. This ensures that your financial reporting is always current, providing a level of clarity that manual processes simply cannot match. It’s about creating a single source of truth for your entire organization.

Synchronizing your payment environment with your accounting software does more than just save time. It transforms your financial data into a live asset. With Intuit announcing price increases for QuickBooks Online subscriptions in August and September 2026, maximizing the value of your existing tech stack is essential. Integrated systems ensure that every ACH transfer and credit card transaction is recorded accurately without the need for a human intermediary, protecting your data integrity and your bottom line.

Automating the Reconciliation Workflow

Manual entry is the enemy of accuracy in high-volume B2B environments. By implementing a QuickBooks ACH Integration Guide, your controller gains immediate visibility into cash flow. Instead of waiting for month-end reports to identify discrepancies, stakeholders can see settled funds and pending transfers as they happen. This transparency allows for more agile decision-making and protects against the errors that inevitably occur when teams are forced to handle repetitive, high-volume data entry across multiple platforms.

Reducing B2B Transaction Costs

Beyond time savings, integration unlocks the ability to transmit Level 2 and Level 3 data automatically. These extra data points, including tax amounts and purchase order numbers, are required by card networks to qualify for significantly lower interchange rates on corporate and purchasing cards. If you aren’t capturing this information, you’re likely paying higher fees than necessary. You can learn more about how to reduce transaction costs for B2B to see the direct impact on your margins. If your current workflow feels fragmented, request a technical consultation to see how a bespoke integration can simplify your operations.

Selecting a Corporate Payment Partner in Wisconsin

Selecting the right provider for your corporate electronic payment services is a decision that extends far beyond comparing fee schedules. In a high-volume environment, you don’t just need a vendor; you need a partner who understands the local economic climate and the specific operational pressures of the Wisconsin market. Whether your firm is based in Milwaukee, Waukesha, or the surrounding areas, having a local mentor ensures your payment architecture is built on a foundation of reliability. It’s about finding a steady hand that offers community-focused accountability alongside technical proficiency.

Local Support for Wisconsin Corporations

Wisconsin’s manufacturing and distribution sectors have unique workflows that generic, national providers often overlook. By working with a consultancy that understands the regional landscape in Milwaukee, Brookfield, and Madison, you can tailor your Ecommerce payment processing for corporations to match your specific supply chain requirements. This local proximity allows for a more responsive relationship, moving beyond clinical support tickets to a partnership grounded in your long-term success. We believe that professional authority should always be accessible to the community it serves.

The Implementation Roadmap

Transitioning from legacy systems to modern corporate electronic payment services requires a methodical approach to ensure continuity. We prioritize a structured roadmap that begins with a deep discovery of your existing QuickBooks workflows and ends with a seamless cutover. Our goal is always minimal downtime, ensuring that your B2B transactions continue to flow without interruption during the integration phase. With over 30 years of industry experience, we guide you through each milestone, providing the strategic leadership necessary to navigate technical nuances and industry standards with confidence.

Future-Proofing Your B2B Payment Strategy

Optimizing your payment infrastructure is a strategic investment that pays dividends in both operational time and liquid capital. By bridging the “Automation Gap” with seamless QuickBooks synchronization and adopting high-volume ACH solutions, your organization can move from reactive compliance to proactive growth. We’ve explored how corporate electronic payment services should serve as a background engine for your business, reducing friction and capturing lower transaction rates through specialized Level 2 and Level 3 data transmission.

With over 30 years of local Milwaukee experience, P2EZPay Merchant Services understands the specific complexities of the Wisconsin corporate landscape. We act as a dedicated mentor, offering specialized B2B cost-reduction strategies and the expertise required for complex technical integrations. If you’re ready to modernize your financial stack and protect your margins within a shifting regulatory environment, it’s time to Schedule a Consultation with P2EZPay Merchant Services for Your Corporate Payment Needs. We’re here to provide the steady leadership and expert guidance needed to build a more resilient and efficient future for your business operations.

Frequently Asked Questions

What is the difference between corporate ACH and standard bank transfers?

Corporate ACH provides a structured data environment that standard bank transfers lack. While standard transfers are often one-off manual actions, corporate ACH utilizes batch processing and CCD or CTX formats to include detailed invoice information. This structure enables automated reconciliation within your accounting software. It’s a more scalable solution for businesses managing high-volume payouts and collections compared to the manual overhead of traditional bank wires.

How does QuickBooks payment integration save money for B2B companies?

Integration saves money by removing the labor costs associated with manual reconciliation. By synchronizing your ledger directly with corporate electronic payment services, you eliminate the need for manual data entry. This reduces administrative hours and prevents costly accounting errors. Additionally, integrated systems automatically capture the enhanced data required for Level 3 processing, which directly lowers the interchange fees you pay on corporate card transactions.

Can I use corporate electronic payment services for international B2B transactions?

Yes, many corporate electronic payment services facilitate international B2B payments through Global ACH or the SWIFT network. These services are often more cost-effective than traditional bank wires, offering more competitive exchange rates and lower flat fees. When managing global vendors, utilizing a unified platform for both domestic and international needs ensures that your financial reporting remains consolidated and that you maintain clear visibility over your cross-border expenditure.

What are Level 2 and Level 3 processing fees in B2B payments?

Level 2 and Level 3 processing involves sending extra data points, like purchase order numbers and tax details, to the card brands. This additional information reduces the perceived risk of the transaction. In response, card networks offer lower interchange rates for B2B and government cards. Without this data, your transactions default to Level 1 rates, which are significantly more expensive and can quietly erode your corporate margins over time.

Is e-check processing safer than traditional paper checks for businesses?

E-check processing is much safer than traditional paper checks because it uses encrypted digital channels rather than physical documents. Paper checks are vulnerable to interception, forgery, and manual alteration at multiple points in the mail and deposit cycle. Digital e-checks are governed by strict 2026 Nacha fraud monitoring requirements, ensuring that every transaction is validated and tracked. This modern approach protects your bank credentials and provides a secure environment for high-value transfers.