What if the very banks you trust to manage your capital are actually the biggest obstacle to your profitability? Most financial leaders agree that managing high-volume transactions often feels like a constant battle against rising costs and inefficient manual data entry. It’s exhausting to deal with opaque fee structures and a lack of dedicated support when you’re trying to scale your corporate payment processing infrastructure. You deserve a partner that acts as a loyal ally rather than a distant vendor.

You’ve likely felt the frustration of watching interchange fees eat into your margins or seeing your accounting team struggle with manual reconciliation. It’s a common pain point that stems from a system designed for the banks, not the merchants. This guide will show you how to flip that script by evaluating providers through a more critical lens, leveraging the latest 2026 standards to lower your costs. We’ll explore how to navigate the recent retirement of Visa’s Level 2 program, utilize Level 3 data to optimize interchange rates, and implement seamless automation for your QuickBooks workflows. By the end of this article, you’ll have a clear roadmap to secure high-volume processing with a partner that values your long-term success.

Key Takeaways

- Understand why high-volume B2B environments require specialized security and data handling that standard consumer processors often lack.

- Evaluate the strategic advantages of choosing an agile payment partner over a traditional big bank to gain more personalized support and transparent fee structures.

- Learn how to leverage Level 3 data to lower interchange costs, a critical step for any business scaling its corporate payment processing operations in 2026.

- Streamline your financial workflows by integrating your payment data directly into QuickBooks, effectively removing the burden of manual reconciliation.

- Shift your perspective from treating payments as a utility to viewing them as a strategic lever for growth through a bespoke partnership approach.

What is Corporate Payment Processing?

Corporate payment processing encompasses the sophisticated ecosystem of B2B transactions, digital commerce, and automated clearing house (ACH) transfers that power modern enterprise operations. It’s the backbone of your financial health. Unlike a simple retail swipe, corporate systems handle complex financial flows that require absolute precision. For a growing Milwaukee enterprise, this infrastructure isn’t just a utility. It’s a strategic foundation. It supports high-volume movement of capital across global supply chains and ensures that local growth isn’t hindered by technical bottlenecks or outdated fee structures.

A professional payment processor acts as more than a middleman in this environment. They serve as a specialized consultant. They understand the nuances of enterprise-level risk and the necessity of seamless data integration. As businesses scale, the ability to process payments efficiently becomes a competitive advantage. It directly impacts cash flow and operational agility. Partnering with an expert allows you to move beyond basic transaction handling to a model that supports long-term fiscal stability.

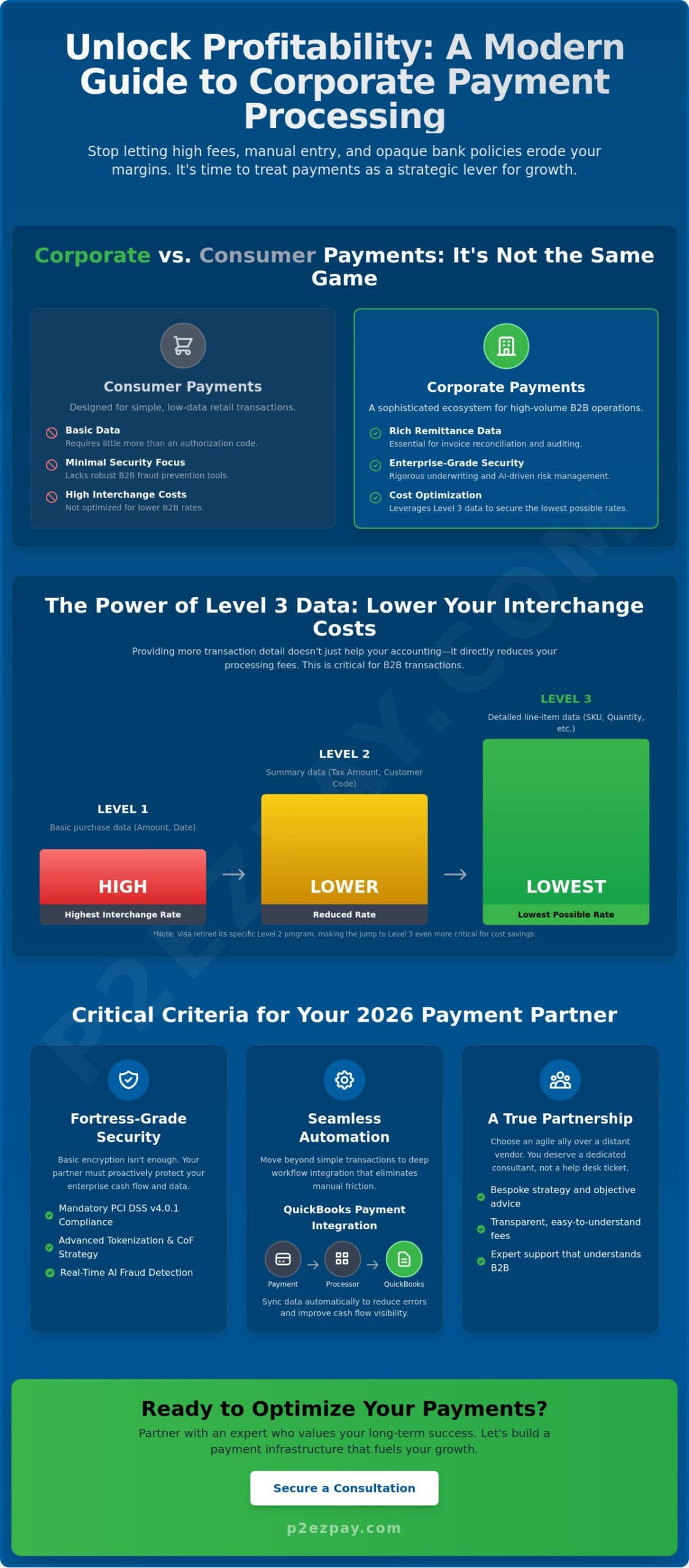

Corporate vs. Consumer Payments: Key Differences

The primary distinction between corporate and consumer payments lies in the scale and complexity of the data involved. High-volume merchant environments don’t just process more transactions. They process larger, more frequent transfers that demand rigorous underwriting and sophisticated risk management. While a consumer payment requires little more than an authorization code, corporate transactions necessitate detailed remittance data. This information is vital for reconciling invoices and maintaining transparent records across complex procurement cycles. Selecting a partner for corporate payment processing requires understanding these technical demands to avoid the pitfalls of consumer-grade solutions.

The Role of a Payment Processor in 2026

By 2026, the expectations for financial partners have shifted. We’ve moved from simple facilitation to deep workflow automation. Modern processors prioritize the removal of manual friction through tools like QuickBooks payment integration. This evolution ensures that data moves securely while maintaining strict adherence to the latest PCI DSS v4.0.1 standards. An independent advisor doesn’t just provide a platform. They offer a bespoke strategy to optimize your corporate payment processing environment. They ensure that security protocols, such as AI-driven fraud detection, protect enterprise data without slowing down legitimate business growth.

Critical Criteria for Choosing a Corporate Payment Partner

Choosing a partner for corporate payment processing shouldn’t be a choice between security and speed. While large national banks offer a sense of institutional stability, they often struggle with the agility required to adapt to specific B2B needs. A boutique consultancy acts as a strategic mentor. They provide the same high-level security but with a level of flexibility that large institutions simply can’t match. This agility is crucial when managing diverse payment methods such as ACH and e-checks, where rules and fraud risks are constantly evolving.

A reliable partner must also stay ahead of regulatory updates, such as the 2026 Nacha rules that emphasize fraud monitoring and internal controls for ACH payments. This level of foresight ensures your business remains compliant and secure without requiring you to become an expert in every technical nuance. When you select a processor that prioritizes independent, objective advice, you’re investing in the long-term resilience of your organization.

Security and Compliance Standards

In 2026, basic encryption is no longer enough to protect enterprise cash flow. Your partner must demonstrate full adherence to the mandatory PCI DSS v4.0.1 requirements that became effective in early 2025. This includes advanced tokenization and Credential-on-File (CoF) strategies to secure sensitive data. With 79% of organizations experiencing attempted or actual payments fraud in 2025, real-time AI risk scoring is now a necessity. These tools analyze transaction patterns instantly to identify anomalies that human review might miss. This proactive stance is the hallmark of a partner that values protection as much as performance.

For organizations looking to extend this level of protection to their broader IT and physical infrastructure, Beyer Bytes offers specialized security solutions that ensure every layer of the business remains resilient against evolving threats.

Support and Consultancy Models

The difference between a vendor and a partner becomes clear when an issue arises. Automated help desks and generic ticketing systems are insufficient for high-volume accounts where every minute of downtime has a financial cost. A dedicated account manager offers a steady hand. They understand your specific business challenges and provide proactive guidance rather than reactive fixes. For companies in the Milwaukee area, having a local authority means access to professional consultancy that understands the regional economic landscape. If you’re looking for a more tailored approach to your financial operations, exploring bespoke corporate payment solutions can help you transition from a vendor-client relationship to a strategic partnership.

Optimizing B2B Costs: The Power of Level 2 and Level 3 Processing

While many financial leaders focus on reducing manual labor, the most significant drain on B2B profitability often remains hidden within interchange fees. Standard corporate payment processing configurations frequently default to Level 1 rates. These rates are designed for simple consumer transactions and carry the highest costs. By providing additional data points during the authorization process, businesses can qualify for Level 2 and Level 3 rates, which significantly reduces the percentage paid to card networks. This optimization is a strategic lever that directly impacts your bottom line.

Qualifying for these lower rates requires a sophisticated approach to data management. For Level 2, you typically need a customer reference number and sales tax information. However, the landscape changed significantly in January 2026 when Visa retired its Level 2 program. To access discounted rates on Visa commercial cards now, merchants must provide full Level 3 data through the Commercial Enhanced Data Program (CEDP). While Mastercard continues to support Level 2, the industry trend clearly favors the deeper transparency of Level 3. A partner who understands these nuances ensures your transactions don’t fall into the most expensive categories by default.

The primary objection to implementing these optimizations is often the perceived “switch cost” or the effort required to update legacy systems. It’s a valid concern for any busy finance department. However, when you compare the one-time transition effort against the long-term interchange savings, the financial logic is clear. A strategic partner helps you navigate this transition by providing the technical framework to automate data capture. This ensures that the long-term savings in corporate payment processing fees far outweigh any temporary operational shift. Organizations that have embraced modern B2B payment automation strategies consistently find that the combination of Level 3 data capture and workflow automation delivers compounding returns well beyond the initial implementation effort.

What is Level 3 Processing?

Level 3 processing requires line-item detail to qualify for the lowest possible B2B interchange rates. This includes specific data such as item descriptions, quantities, unit costs, and freight amounts. Modern automated systems capture this information directly from your invoices, removing the need for manual entry and reducing the risk of human error. For high-volume merchants, this level of detail doesn’t just save money; it transforms the merchant account into a high-performance financial asset that supports scalable growth.

Comparing Interchange Optimization Strategies

Choosing between wholesale pricing and tiered models is a critical decision for corporate environments. Tiered pricing often obscures the true cost of transactions by bundling them into broad, expensive categories. Wholesale (interchange-plus) pricing is more transparent, allowing you to see exactly how much you’re paying to the card networks versus your processor. Conducting a thorough B2B payment cost analysis can expose hidden fees and identify where optimization is most needed. Integrating ACH and e-check solutions alongside your card processing can further reduce costs for recurring or high-value transactions where credit cards aren’t the most efficient option.

Workflow Automation: QuickBooks Payment Integration

Efficiency in corporate payment processing is measured by how little your team has to touch each transaction. When your payment gateway and accounting software operate in silos, you’re forced to bridge the gap with manual labor. This creates delays and increases the risk of reconciliation errors that can haunt your year-end audits. True workflow automation begins when your payment data flows seamlessly into your general ledger; it transforms a tedious administrative task into a quiet background process that supports your broader financial goals. A well-executed B2B payment integration with accounting software is the foundation of this transformation, connecting your transaction data directly to your financial records without manual intervention.

Eliminating Manual Data Entry

Manual entry is the enemy of scale. High-volume environments can’t afford the luxury of manual data entry, where every keystroke is an opportunity for error. This is especially true when dealing with complex B2B remittance data. A direct integration ensures that when a payment is processed, it’s immediately recorded and applied to the correct invoice. This level of synchronization simplifies daily reconciliation and provides your finance team with accurate, up-to-the-minute reporting. By removing the friction of manual entry, you allow your staff to focus on strategic analysis rather than data correction.

Improving Cash Flow Management

Real-time visibility is the foundation of sound fiscal leadership. Integrated corporate payment processing solutions provide the clarity needed to manage high-volume cash flows effectively. When your payments are integrated with QuickBooks, you gain an immediate view of your corporate liquidity. For businesses that need to consolidate data from various financial institutions, using a banking aggregation API like Wealthreader can further enhance this visibility. You can see exactly which invoices are outstanding and which have been settled without waiting for a manual update at the end of the week. This transparency is vital for accurate forecasting and making informed decisions about capital allocation. Leveraging these integrated workflows often leads to faster settlements, as the system can automatically handle multi-invoice payments, a feature standardized in the April 2026 QuickBooks update.

If you’re ready to modernize your financial stack and eliminate administrative bottlenecks, you can automate your QuickBooks reconciliation today with our bespoke integration tools.

Before committing to a provider, use this checklist to evaluate the integration’s reliability and speed:

- Sync Speed: Does the data update in real-time or through delayed batches?

- Bi-directional Mapping: Can the system sync both ways to ensure invoices and payments are always aligned?

- Multi-Invoice Support: Can customers pay multiple invoices in a single transaction to simplify the checkout experience?

- Security Standards: Does the integration maintain full PCI DSS v4.0.1 compliance during every data transfer?

- Error Handling: How does the system manage and alert your team to failed sync attempts?

Partnering with a Milwaukee Corporate Payment Expert

While the technical nuances of interchange optimization and software integration are vital, the most critical component of a successful financial strategy is the partnership behind it. Large, impersonal institutions often treat corporate payment processing as a generic utility. They provide the basic infrastructure but lack the strategic leadership needed to adapt to your specific business model. A local Milwaukee expert offers a different experience. We act as a seasoned mentor, providing a steady hand through complex transitions and offering protection against the rising costs of B2B transactions.

Choosing a partner is about finding an ally who’s deeply invested in your journey. At P2EZPay, we shift the relationship from a standard vendor model to a long-term strategic partnership. This transition begins with a transparent onboarding process designed to minimize operational downtime. We handle the technical heavy lifting, ensuring that your transition to a more efficient processing model is seamless and secure. It’s a methodical approach that prioritizes your comfort and security at every stage.

The P2EZPay Advantage

Our team brings over 30 years of experience as independent payment consultants to the Milwaukee business community. We specialize in high-volume merchant services and deep QuickBooks integration, focusing on the specific needs of regional enterprises. Because we’re independent, we offer objective advice that prioritizes your profitability over bank margins. We understand the local market and the unique challenges faced by Wisconsin based companies. This local perspective allows us to provide a level of accessibility and tailored support that national banks simply can’t replicate.

Next Steps: Evaluating Your Current Statement

The path to lower costs begins with a clear understanding of your current financial landscape. We invite you to request a complimentary merchant account optimization audit. During this session, we’ll analyze your existing statements to identify hidden fees and missed opportunities for Level 3 interchange savings. Preparing your data for this transition is straightforward, and our team will guide you through every step. If you’re ready to reclaim your margins and secure a more reliable financial future, contact P2EZPay today for a tailored B2B payment analysis.

We take pride in acting as a loyal ally for our clients. Whether you’re dealing with the complexities of corporate payment processing for the first time or looking to optimize an existing high-volume account, we’re here to provide the strategic leadership your organization deserves. Schedule your professional consultancy session today to see how a bespoke approach can transform your financial workflows and support your long-term success.

Securing Your Financial Future Through Strategic Partnership

We’ve explored how a shift in your perspective on payments can unlock significant corporate capital. Efficiency is your greatest asset. By moving beyond basic Level 1 processing and embracing the line-item detail required for Level 3 rates, you aren’t just saving on fees; you’re strengthening your organization’s bottom line. Integrating these financial flows directly into your accounting software removes the persistent friction of manual entry. This allows your team to focus on high-level growth and strategic analysis. In a complex financial landscape, having a steady hand to guide your corporate payment processing strategy is essential for long-term stability.

P2EZPay brings over 30 years of industry experience to help you navigate these technical nuances. We specialize in Level 2 and Level 3 interchange optimization and offer dedicated QuickBooks integration support. We’re committed to acting as your loyal ally, providing the professional consultancy needed to remove obstacles and streamline your operations. Your success is our mission.

Optimize Your Corporate Payment Strategy with P2EZPay and take the first step toward a more transparent, profitable future. We’re ready to support your journey with expertise and reliability.

Frequently Asked Questions

What is the difference between a payment gateway and a corporate merchant account?

A payment gateway is the digital infrastructure that captures and transmits transaction data, while a corporate merchant account is the specialized bank account where funds are held before being settled into your business bank. You need both to accept digital payments effectively. The gateway ensures security during transmission, whereas the merchant account manages the risk and settlement of your capital.

How much can Level 3 processing actually save my B2B business?

Level 3 processing significantly reduces your interchange costs by providing card networks with detailed line-item data for each transaction. While specific savings vary based on your volume and card mix, B2B transactions often qualify for much lower rates than standard Level 1 processing. This is particularly relevant now that Visa requires Level 3 data via the Commercial Enhanced Data Program (CEDP) to access discounted commercial rates.

Can I integrate my existing QuickBooks Desktop with a new payment processor?

You can integrate your existing QuickBooks Desktop software with a new payment processor to streamline your financial data. Most modern integrations for QuickBooks Desktop include interchange optimization features that automatically add Level 2 and Level 3 data to your B2B transactions. This removes the need for manual reconciliation and ensures that your accounting records remain perfectly synchronized with your actual cash flow.

Is ACH processing safer than credit card processing for high-volume B2B?

ACH processing is highly secure for high-volume B2B transactions, especially with the introduction of Nacha’s 2026 rules that emphasize real-time validation and fraud monitoring. While credit cards offer robust protection through PCI DSS v4.0.1, ACH is often preferred for larger B2B transfers due to its lower cost and direct bank-to-bank nature. Both methods provide reliable security when managed by a partner that prioritizes internal controls and data protection. For a deeper look at how to automate and secure these transfers within your accounting system, our guide on QuickBooks ACH integration for B2B payment automation covers the latest 2026 NACHA compliance requirements in detail.

How long does it take to switch corporate payment processing providers in Milwaukee?

Switching corporate payment processing providers in Milwaukee typically takes between three to seven business days. This timeline depends on the complexity of your current setup and the speed of your existing software integrations. A local partner provides a methodical onboarding process to ensure that your transition is handled with care and that there is no disruption to your daily operations or cash flow.

What security standards should I look for in a high-volume payment gateway?

Look for a gateway that maintains full compliance with PCI DSS v4.0.1 and utilizes advanced tokenization to protect sensitive information. High-volume environments also require real-time AI risk scoring to detect and block evolving fraud patterns before they impact your business. These standards ensure that your enterprise-level data remains secure while supporting the rapid movement of high-value transactions across your B2B portals.

What are the most common hidden fees in corporate payment processing?

The most common hidden fees include PCI non-compliance charges, monthly statement fees, and undisclosed markups on tiered pricing models. Many processors also hide costs within batch header fees or annual regulatory compliance surcharges. Working with an independent advisor helps you identify these opaque structures in corporate payment processing and transition to a more transparent interchange-plus pricing model that clearly outlines every cost associated with your account.