Reduce credit card processing fees is a goal that sits at the top of the priority list for a lot of business owners once they actually look at what those fees are costing them every month. The first time many business owners pull a detailed report on their processing costs, the number surprises them.

It’s not one fee. It’s a layered structure of interchange rates, processor markups, monthly fees, batch fees, chargeback fees, and a handful of other line items that quietly add up to a significant monthly expense. I’ve spoken to small business owners paying two to four percent on every card transaction without really understanding what’s driving those costs or what they could do about them. At P2EZPay, we help businesses understand their payment costs and find legitimate ways to reduce them without compromising the customer experience or taking on unnecessary risk.

Why Credit Card Processing Fees Are Higher Than They Need to Be

Most businesses accept whatever fee structure their processor offers them at signup without questioning it. Processors know this. The default pricing they offer new merchants is rarely their most competitive offering and it often includes markup layers that can be negotiated down or eliminated entirely.

Understanding the fee structure is the first step toward reducing it. Processing fees have three main components. Interchange fees set by card networks like Visa and Mastercard. Assessment fees charged by those same networks. And processor markup, which is where most of the negotiation opportunity exists.

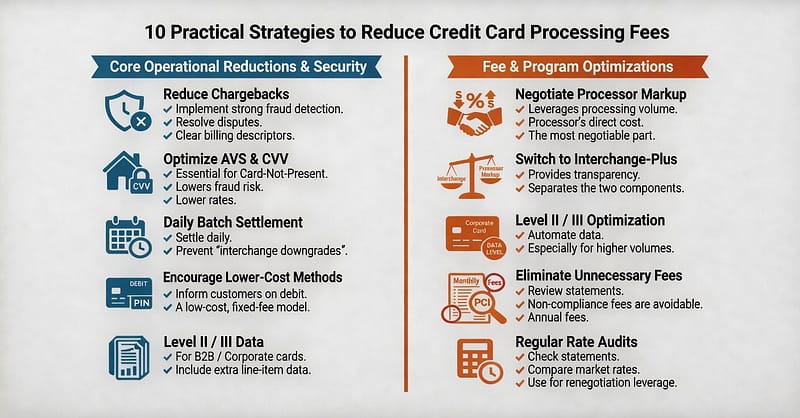

10 Practical Ways to Reduce Credit Card Processing Fees

These are methods that actually work in real business environments rather than theoretical suggestions that don’t hold up in practice.

1. Negotiate Your Processor Markup

The processor markup is the component of your fees that your payment processor controls directly. It is also the most negotiable part of your cost structure. Processors compete for business and most have flexibility in their pricing that they won’t volunteer unless you ask.

Before negotiating, pull together your monthly processing volume, your average transaction size, and your current effective rate. Processors respond better to specific data than to general requests for lower fees. A business processing significant volume has meaningful leverage in that conversation.

At P2EZPay, we work with businesses to review their current processing costs and identify where reduction is genuinely achievable through better pricing structures.

2. Switch to Interchange-Plus Pricing

Many businesses are on flat-rate or tiered pricing models that bundle interchange fees with processor markup in a way that obscures what you’re actually paying. Interchange-plus pricing separates the interchange cost from the processor markup and shows you each component clearly.

For most businesses with moderate to high volume, interchange-plus pricing results in lower total costs than flat-rate pricing because you pay the actual interchange rate for each transaction rather than a blended rate that averages across all card types.

3. Encourage Lower-Cost Payment Methods

Different payment methods carry different interchange rates. Here is a general comparison:

| Payment Method | Typical Interchange Range | Notes |

| Debit card (PIN) | 0.05% to 0.80% | Lowest cost option |

| Debit card (signature) | 1.15% to 1.80% | Higher than PIN debit |

| Standard credit card | 1.50% to 2.30% | Mid-range cost |

| Rewards credit card | 1.80% to 3.00% | Higher due to reward funding |

| Corporate/purchasing card | 2.50% to 3.50% | Highest interchange rates |

Businesses that inform customers about lower-cost payment options or implement cash discount programs reduce their average interchange cost across the total payment mix without refusing any payment method.

4. Implement Address Verification and CVV Requirements

Transactions that include address verification and CVV data qualify for lower interchange rates in many card categories because they carry lower fraud risk. Businesses that collect this data consistently on card-not-present transactions reduce their interchange costs on those transactions and reduce chargeback exposure simultaneously.

For eCommerce businesses, making address verification and CVV fields required rather than optional is a straightforward change that affects interchange qualification on every eligible transaction.

5. Settle Transactions Daily

Transactions that aren’t settled within a certain timeframe after authorization can downgrade to higher interchange rate categories. Daily batch settlement ensures authorized transactions settle before any downgrade window closes.

This is particularly relevant for businesses that sometimes delay batch settlement because they’re busy or because their setup doesn’t settle automatically. Configuring automatic daily settlement costs nothing and prevents unnecessary interchange downgrades on transactions that would otherwise qualify for lower rates.

6. Evaluate and Upgrade Your Payment Hardware

Older terminals can sometimes lead to higher costs because they lack modern security features or don’t support faster, cheaper transaction types like contactless payments (NFC). Using up-to-date, EMV-compliant hardware ensures that your transactions are processed at the most secure and cost-effective level. Modern systems also help automate tracking, which prevents errors that lead to extra fees.

7. Reduce Chargebacks

Chargebacks cost money beyond just the disputed transaction amount. Chargeback fees from processors typically run between fifteen and one hundred dollars per incident. High chargeback rates also trigger higher processing rates or merchant account termination in serious cases.

Reducing chargebacks requires clear billing descriptors that customers recognize on their statements, robust customer service that resolves disputes before they become chargebacks, and fraud screening tools that catch fraudulent transactions before they process. Each of these reduces chargeback frequency and the associated costs.

8. Avoid Keyed-In Transactions Where Possible

Transactions where card data is manually keyed in rather than read from the card carry higher interchange rates than card-present swiped or tapped transactions. They also carry higher fraud risk which contributes to the higher rate.

For businesses that regularly key in transactions because their setup makes card-present transactions inconvenient, reviewing the payment hardware or software setup to enable card-present processing more often reduces the interchange cost on those transactions.

9. Review and Eliminate Unnecessary Fees

Monthly statements often include fees that aren’t related to interchange or processor markup. Monthly minimum fees, statement fees, PCI non-compliance fees, batch fees, and annual fees all add to total processing costs without being directly connected to transaction volume.

PCI non-compliance fees are particularly worth addressing. Merchants who have not completed their PCI compliance self-assessment on an annual basis incur these fees. Finishing the evaluation removes the charge while simultaneously keeping the company in the clear with its compliance duties.

P2EZPay reviews merchant statements in detail to identify fee line items that can be reduced or eliminated as part of our client onboarding process.

10. Shop Competing Processors Regularly

The payment processing market is competitive and pricing changes over time. A processor that offered competitive rates three years ago may no longer be the best option available today. Reviewing competing offers every couple of years ensures the business isn’t paying a loyalty premium to a provider that has been undercut by alternatives.

Getting competing quotes doesn’t require switching processors immediately. It gives the business accurate current market pricing to use as a benchmark and as leverage in renegotiation conversations with the current processor.

FAQs

Q: What is a realistic fee discount that a business can get?

It depends on your current fee structure and volume, but businesses on inefficient pricing models often cut their total processing costs by 20-40% by utilizing several of these strategies in conjunction.

Q: Is interchange-plus pricing better than flat-rate pricing?

For businesses with moderate-to-high volumes, it generally would be. For businesses with very low volumes, flat-rate pricing can make more sense than interchange-plus, despite the latter’s cost advantage.

Q: What is a PCI compliance fee & how can I avoid it?

A fee applied by the processors to merchants who don’t complete their annual self-assessment questionnaire for PCI compliance. The fee will be waived if the questionnaire is completed.

Q: How often should a business review its processing fees?

At least once a year. Reviewing more often makes sense when the volume processed changes significantly, or the terms of the contract allow for renegotiation.

Do cash discount programs really reduce processing fees?

Indeed, when done correctly, the answer is affirmative. Through this approach, businesses are able to shift the costs of card acceptance to the customers who choose to use cards, as opposed to cash, with the result being a lowering of the net processing cost of the concerned business.

Conclusion

Credit card processing fees can be reduced for almost any credit card accepting business once you fully understand the fee structure and apply the available strategies on a consistent basis. No one way abolishes processing costs, but several of them can help reduce processing costs in meaningful amounts that will add up to a significant amount of savings each year at any reasonable level of transaction volume.

The businesses that treat payment processing costs as a manageable expense rather than a fixed cost of doing business consistently spend less than those that accept the default pricing and never revisit it. If you want a detailed review of your current processing costs and practical guidance on where reduction is achievable for your specific business, visit P2EZPay and talk to a team that helps businesses reduce credit card processing fees through better pricing structures and smarter payment strategies every single day.