Credit card processing fees are a silent killer of your profit margins. With many businesses paying corresponding fees in the range of 1.5 to 3.5 percent per transaction, they add up fast. The good news? With the proper tactics, you can cut a huge chunk off the cost of what you pay while keeping more revenue in your pocket.

In this guide, we’ll explain proven expert-backed ways to decrease your credit card processing costs whether yours is a small retail shop, B2B concern, or high-volume vendor.

What Are Credit Card Processing Fees?

You can’t cut fees until you know what you’re paying. Credit card processing fees generally have three parts:

- Interchange: Fees charged to the merchant by the bank that issues the card (Visa, Mastercard, Amex). These are constants, but they can be min/maxed.

- Assessment fees: Minor charges assessed by the card networks themselves.

- Processor margin: The cost a payment processor adds on top of this. This is where your negotiating leverage is greatest.

Common Fee Structures

| Fee Model | How It Works | Best For |

| Flat Rate | Same % on every transaction (e.g., 2.9% + $0.30) | Small/new businesses |

| Interchange Plus | Interchange cost + fixed processor markup | Mid to large businesses |

| Tiered Pricing | Transactions bucketed into “tiers” (qualified, mid, non-qualified) | Often the most expensive avoid if possible |

| Subscription/Membership | Monthly fee + low per-transaction cost | High-volume merchants |

Step 1 is to understand your existing fee model. If you’re on a tiered pricing model, switching alone may save you thousands of dollars per year.

1. Negotiate Directly With Your Payment Processor

It’s a fact that escapes many business owners: Processor markups are negotiable. Your processor’s margin (not the interchange) is what can be negotiated.

What to do:

- Ask for an itemized fee statement and determine the percentage of markup.

- Use competitor quotes as leverage.

- Request an interchange-plus pricing model, which is more transparent and generally cheaper than tiered pricing.

At P2EZPay, our non-biased merchant consultants review your current statements and negotiate on your behalf, usually getting you a better rate without having to change processors.

2. Encourage Lower-Cost Payment Methods

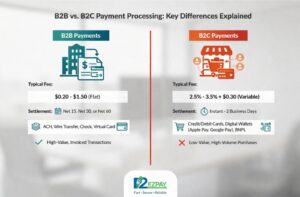

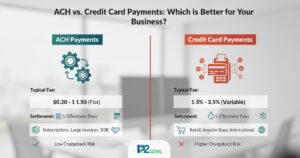

Not all transactions are created equal. Debit transactions have lower associated fees than credit cards. Corporate or rewards cards tend to have higher interchange rates.

Smart steps:

- Give a slight discount to customers who pay with debit or ACH/bank transfer.

- If you are a B2B merchant, work towards obtaining Level 2 and Level 3 processing (more on that later).

- Contemplate surcharging programs where permissible let consumers who select premium cards pay the gap.

3. Use Level 2 and Level 3 Processing for B2B Payments

If your business targets other businesses or government agencies, Level 2 and Level 3 card data processing can help cut interchange rates significantly.

Submit more transaction data (such as purchase order numbers, tax amounts, and line-item details) to receive lower interchange tiers established by Visa and Mastercard.

Potential savings: B2B businesses can save between 0.5% and 1.5% per transaction in interchange costs, a huge deal when you’re making big orders.

P2EZPay is an expert in B2B payment processing, and it helps businesses to pass Level 2/3 data automatically, so you can enjoy these savings.

4. Avoid Manual Key-Entry Transactions

Face-to-face (card present) transactions are assumed to be less risky because the cardholder is present and warrants lower interchange fees. Transactions keyed in by hand known as manual key-entered transactions and often taken over the phone are considered more risky and are charged a higher fee.

Best practices:

- Card Readers: Always use a card reader in front of the customer.

- Use discounting and tokenization (and AVS in ecommerce transactions) to minimize those risk indicators and potential downgrades!

- Don’t split transactions or try several declined cards multiple times.

5. Reduce Chargebacks

In addition, chargebacks don’t just cost you a sale, they typically include fees of between $20 and $100 per incident, along with potential increases to your processing rate if your chargeback ratio becomes too high.

How to reduce chargebacks:

- Utilize clear billing descriptors (meaning, use your business name as customers know it).

- Send order confirmation emails and delivery tracking.

- To Provide a clear, easy-to-find refund policy.

- Leverage fraud detection tools and AVS/CVV for card-not-present transactions.

6. Batch Transactions Daily

You’ll be required to “[batch]” or settle your transactions within 24 hours in most cases. If you sell after 24 hours, some of your transactions may be downgraded to a higher fee tier. Implement daily batch sweeping in your POS or processor to stop fee creep.

7. Review Your Statements Every Month

Fee structures can change. Processors sometimes quietly adjust rates or add new fees. Set a reminder to review your processing statements monthly.

What to look for:

- Unexpected fee line items

- Increase in non-qualified transaction volume

- PCI non-compliance fees (often avoidable just complete your annual PCI questionnaire)

If your statement is confusing, an independent payment consultant like P2EZPay can review it for free and flag savings opportunities.

8. Consider a Cash Discount or Surcharge Program

Cash discount programs provide consumers with a small discount for using cash as payment, effectively shifting the burden of card acceptance to cardholders. A surcharge program tacks a small fee (capped at 4% by card networks) onto what customers pay when they use their credit card.

Most U.S. states allow these programs, and they can be used to completely avoid or reduce your processing costs significantly.

Note: Rules vary by state and card network. Never surcharge without consulting an experienced payment advisor.

Why Work With an Independent Payment Consultant?

There’s a big difference between an independent merchant services advisor (like P2EZPay) and the affiliated processors or mega-players in payment processing — we work for you, not the card networks. We:

- Free auditing of your current processing statements

- Reveal hidden charges and billing mistakes.

- Negotiate with processors for you directly.

- Advise on the correct pricing model for your capability, volume, and business type.

- Aid you in setting up legal surcharge or cash discount programs.

- What we’re looking for: money in your pocket.

Frequently Asked Questions (FAQs)

Q: What is the average credit card processing fee for small businesses?

A: It varies by processor, but the average is between 1.5% and 3.5% per transaction, with some falling outside this range on either side (although that’s rare).

Q: Can I negotiate credit card processing fees?

A: Yes, markup costs for the processor are negotiable. As per Visa/Mastercard, they are not, but can be optimized with Level 2/3 processing and good transaction handling.

Q: What is interchange-plus pricing?

A: The name of the game is transparent pricing – you pay an interchange plus rate, which simply means you’re paying the interchange cost (actual card rate) and a flat fee for your processor. It’s typically cheaper and more predictable than tiered pricing.

Q: Is surcharging credit card fees legal?

A: Yes, in most of the United States, anyway; a handful of states do not allow surcharging (among them, Connecticut and Massachusetts). And card networks also dictate how it’s implemented. Always consult an expert.

Q: How often should I review my processing fees?

A: Monthly. Processors can adjust rates or add fees, and identifying problems early prevents the possibility of overpaying. Try an annual audit with an independent adviser.

Final Thoughts

Lowering your credit card processing fees is not a matter of playing games or trying to outsmart the system it’s about knowing how things work and making good strategic decisions. The little things (sg). From switching pricing models to the addition of level 2/3 data for b2b transactions, all these small steps can get you a real saving.

At P2EZPay, our goal is to assist companies of all sizes throughout the U.S. in minimizing their cost for payment processing costs. Call us today for a complimentary statement analysis to see how much you can save.