B2B vs B2C payment processing are not the same. If you run a business or manage payments, you really need to understand how these two are different. The way money moves, the time it takes, the tools used everything changes depending on who is paying whom. Get this wrong and you could face serious cash flow problems, long delays, or expensive mistakes. Whether you sell to companies or to everyday customers, your payment setup must match your business type. This blog breaks down every major difference in plain language. No complicated terms. Just straight talk.

What Is B2B Payment Processing?

B2B means business to business. One company pays another company. Think about a clothing brand that buys fabric from a supplier every month. Or a software company that charges another business for using its platform. These are B2B transactions. The payment amounts are usually large. The process involves more steps, and getting paid can take a long time.

B2B payment processing plays a major role in managing business cash flow, vendor relationships, and financial operations. Efficient payment systems help companies reduce delays and improve overall financial management.

B2B payment processing manages all of this from start to finish from sending the invoice to receiving the final payment.

Common B2B payment methods include:

- Bank wire transfers

- ACH payments

- Business checks

- Purchase orders

- Net terms such as Net 30, Net 60, or Net 90

What Is B2C Payment Processing?

B2C means business-to-consumer. A business sells directly to a regular person. You order something online. You pay at a grocery store. So, you subscribe to an app. All of these are B2C. The buyer sees a price, pays right away, and that is it. No invoices. No waiting for approval. So, no back and forth.

Modern B2C payment processing focuses on customer convenience, secure transactions, and seamless checkout experiences across mobile and desktop devices.

B2C is built for speed. The whole experience is designed to be quick and easy for the customer.

Common B2C payment methods include:

- Credit and debit cards

- Digital wallets like Apple Pay or Google Pay

- Buy Now Pay Later options

- Standard online checkout

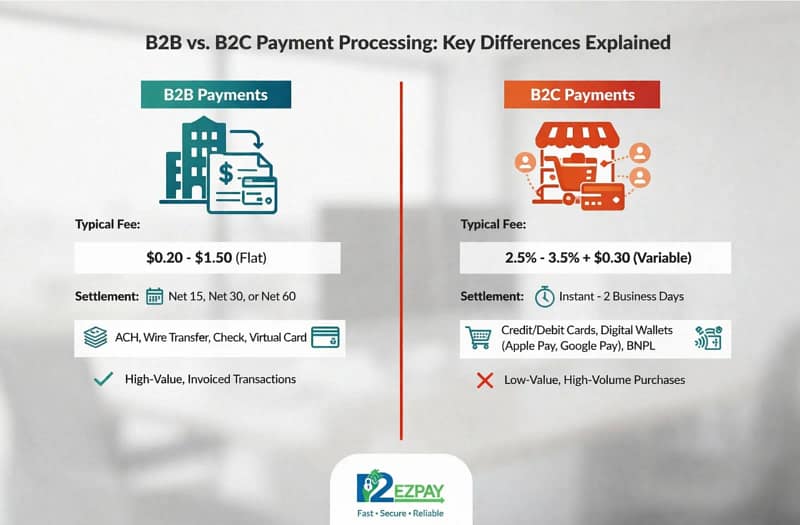

B2B vs B2C Payment Processing: Quick Comparison

| Feature | B2B Payment Processing | B2C Payment Processing |

| Transaction Size | Large, often thousands or more | Small, usually a few dollars to hundreds |

| Payment Speed | Slow, takes days or even weeks | Fast, happens in seconds |

| Payment Methods | ACH, wire transfers, checks, invoices | Cards, wallets, BNPL |

| Billing Cycle | Net 30, 60, or 90 days | Paid instantly at checkout |

| Number of Buyers | Few buyers but high transaction value | Many buyers with lower value per sale |

| Fraud Risk | Less frequent but much higher stakes | More frequent but lower amounts |

| Approval Process | Involves finance teams and managers | No approval needed, direct purchase |

Key Differences Between B2B and B2C Payments

1. Transaction Size and Volume

In B2B, a single payment can easily be worth tens of thousands of dollars. Some deals go even higher. But the total number of transactions per month is usually small.

This is not the case in B2C. You may process thousands daily transactions, but the amounts each is for are small.

This gap matters more than most people realize. Large B2B payments are watched more carefully by banks. More verification steps come into play. You simply cannot treat a fifty thousand dollar wire transfer the same way you treat a fifteen dollar online purchase. The risk levels are completely different.

2. How Fast Payments Actually Move

B2C payments move fast. A card is used, the payment is approved, and money starts moving within seconds. B2B is a whole different situation. A seller sends an invoice. The buyer’s team looks it over. Someone has to approve it. The finance department processes it. Then payment is finally scheduled and sent. This process can take thirty, sixty, or even ninety days from start to finish.

That long wait is a real problem for many businesses. Sales can be strong but cash in the bank stays low because payments are stuck in the pipeline.

Visit P2EZPay Merchant Services to see how their payment tools help businesses get paid faster and manage cash flow better.

3. Payment Methods Are Very Different

Go to any online store and you will find card logos, PayPal, Apple Pay, and similar options everywhere. That is the B2C world. The whole checkout experience is built around making it fast and easy for the buyer.

B2B uses a completely different set of methods. Paper checks are still very common in many industries. ACH bank transfers are widely used. Large international transactions go through wire transfers. Purchase orders, credit lines, and formal payment agreements also play a big role.

These methods are slower but they come with proper documentation and legal protection. That matters a lot when large sums of money are involved.

Many businesses now use integrated payment gateways that support ACH transfers, credit card payments, invoicing, and automated reconciliation from a single platform.

4. Invoicing and the Approval Process

There is no invoice in B2C. You see the price, you pay it, and you are done. B2B invoicing is a proper process on its own. The seller generates an invoice that clearly lists the product or service, their quantity, their price, taxes, and payment terms. That invoice goes to the buyer. The buyer’s finance team checks every line item carefully. An authorized person has to approve it. Then it moves to accounts payable. The payment is processed only after the successful verification of all essential conditions of the transaction.

Indeed, it’s sluggish. However, there’s a goal behind every footstep. It guarantees that neither side will take advantage of the other.

5. Relationships and Long-Term Contracts

Most B2C transactions are one-time or repeat purchases. The business usually has no personal relationship with the buyer. Millions of customers come and go, and that is perfectly fine.

B2B works very differently. Companies build real relationships over time. They sign contracts. They talk about the charges and terms of payment. Delivery schedules are decided in advance. A business may have the same supplier or service provider for many years.

Payments are made differently because of that relationship. Trusted partners are granted credit terms. Some suppliers offer discounts for early payment. Penalties apply for overdue payments. Everything is organized, documented, and connected to the ongoing relationship between the two companies.

6. Tax Rules and Compliance

B2B tax situations can get complicated quickly. Numerous B2B dealings are eligible for tax relief. For instance, a business that buys goods for resale may not owe sales tax. The proper documentation such as exemption certificates and registered tax IDs proves the same.

B2C is much more straightforward. The customer pays the price shown, taxes included. The business collects it and passes it on to the government.

That said, both B2B and B2C businesses must follow financial regulations and banking rules. B2B simply has more layers that need to be dealt with. Compliance errors can result in fines, audits, complicated issues, and more.

7. Fraud and Chargebacks

B2C businesses deal with chargebacks regularly. A customer disputes a charge, the card company investigates, and the merchant often ends up losing even when the sale was completely legitimate. It is a constant challenge for online stores and service providers.

When B2B fraud happens, it’s less common but when it does it causes much more damage. Successful fake invoice, business email compromise, and vendor impersonation attacks result in huge financial losses.

According to the Association of Financial Professionals, more than 70 percent of organizations have been targeted by payment fraud in recent years. B2B businesses need strong verification systems and proper fraud detection tools in place.

Advanced fraud detection tools, payment verification systems, and transaction monitoring help businesses reduce financial risks and maintain payment security.

How to Pick the Right Payment Processor

Your payment processor should match the way your business actually runs.

If you run a B2B business, look for these things:

- Support for ACH transfers and wire payments

- Invoice creation and management features

- Ability to safely handle large transactions

- Options for Net terms or business credit lines

If you run a B2C business, focus on these:

- Card payments and digital wallet support

- A fast and mobile-friendly checkout experience

- Strong built-in fraud protection

- Simple refund and dispute handling

A lot of businesses today deal with both B2B and B2C customers. For them, having one platform that handles everything cleanly is the smartest move.

FAQs

Why do B2B payments require more time?

B2B payments include several stages of payment processing, such as invoice validation, approvals and processing of accounts payable that may increase the time it takes for the money to be released.

Are B2B payments more expensive than B2C ones?

It depends on the payment type. Wire transfers and ACH are charged differently compared to credit cards, as well as bigger transactions may have extra processing fees.

What is meant by ACH in relation to B2B payments?

ACH means Automated Clearing House. This system provides electronic payments from one bank account directly to another one.

How can businesses make their B2B payment cycle faster?

It is possible to decrease delays during the payment processing due to automation of the billing process, approvals and payments from the customer’s side.

Is it true that digital wallets gain popularity in B2B payments?

Yes. Although the most popular types of payments in the B2B sector are bank transfer and cards, digital wallets are slowly gaining popularity there.

Conclusion

If you want to be taken seriously as a business, it’s essential to understand B2B payment processing. There is a lot more than who is buying in the differences between B2B and B2C. There are differences in terms of speed, methods, risks and compliance rules for each sector.

B2B is slow, formal, and relies heavily on trust and documentation. ”B2C is quick, easy, and focused on consumer efficiency.” It is essential to have adequate systems for both.

Modern payment platforms are making things easier, which is a good thing. Manage invoices, accept various types of payments, reduce your risk of fraud, and remain compliant from one place.

Pick the right processor for your business. Design a payment system that matches your real-life working style. Make sure that B2B payment processing benefits your business instead of slowing it down or otherwise.