When comparing ACH vs credit card payments, if you have ever sat down and really looked at your monthly processing fees, you know the frustration. The numbers quietly eat into your margins, and most business owners do not realize how much they are losing until it is too late. That is usually the moment people start asking the real question; should I be using ACH, credit cards, or both? The answer is not black and white, and honestly, it depends on how your business actually operates day to day. Before we get into it, check out https://p2ezpay.com/ for payment solutions built around what businesses actually need.

Let’s Start With the Basics: What Even Is ACH?

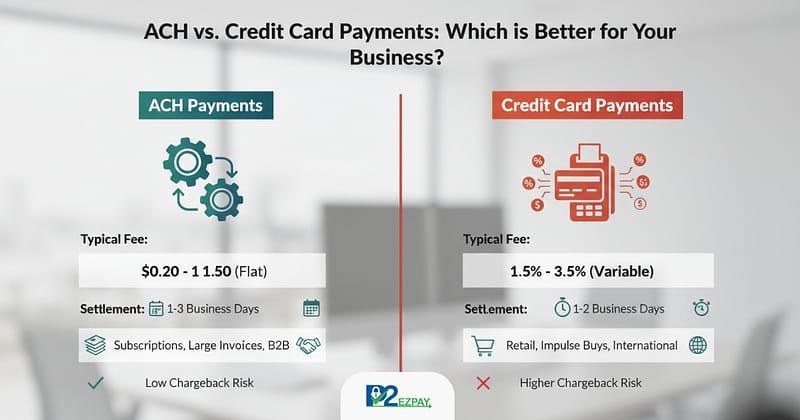

ACH stands for Automated Clearing House. Think of it as a direct line between two bank accounts. When someone pays you through ACH, the money moves from their account to yours through a network of banks; no card company sitting in the middle, no percentage being skimmed off the top.

It is the same system behind your employee payroll, your monthly insurance premium, and your Netflix subscription. You probably use ACH more than you realize, just without thinking about it.

The one thing ACH is not known for is speed. Standard transfers take one to three business days. Same-day ACH exists, but it costs a little more. For most recurring or scheduled payments, though, the timing works out just fine.

And Credit Card Payments: Here Is the Reality

You can get credit cards readily. Your consumers know them, trust them and removing that functionality could realistically mean fewer sales for you. That convenience is real and it’s worth something.

The snags come from the fact that every time a customer sweeps, taps or enters their card number, a percentage of the sale is divided up between the card network, the issuing bank and your payment processor. The card type and your agreement will matter, but we are talking anywhere from 1.5% to 3.5%.

On a $50 sale, that barely registers. On a $5,000 invoice? That is up to $175 gone before you see a cent of it.

ACH vs Credit Card Payments: The Cost Breakdown

This is where most business owners have their “aha” moment. Let’s put it side by side so it actually makes sense:

| Feature | ACH Payments | Credit Card Payments |

| Typical Fee | $0.20 – $1.50 flat rate | 1.5% – 3.5% per transaction |

| Monthly Fees | Sometimes | Often |

| Chargeback Risk | Low | Noticeably Higher |

| Settlement Time | 1–3 business days | 1–2 business days |

| Best Fit | Large, recurring, B2B | Retail, impulse, consumer |

| Customer Experience | Slightly more steps | Fast and familiar |

When you lay it out like this, the ACH vs Credit Card Payments conversation becomes much clearer; it is not really about which one is “better,” it is about which one makes sense for a given type of transaction.

Situations Where ACH Just Makes More Sense

Nobody is going to tell you to drop credit cards entirely. But there are specific situations where ACH is clearly the smarter call:

- You are dealing with large invoices: If you are billing clients $2,000, $5,000, or more at a time, the math on credit card fees gets painful fast. ACH keeps that cost to almost nothing.

- You run any kind of subscription model: Monthly billing, annual plans, retainer agreements; ACH handles all of this quietly in the background. No card expiration dates to chase down, no failed payment emails to send.

- Your customers are other businesses: B2B payments are a natural fit for ACH. Most businesses have no problem authorizing a direct bank transfer, especially when it saves everyone money.

- Processing payroll is typically done by ACH because it is faster and more secure. It has been proven to be reliable, traceable and cost-effective at scale.

Situations Where Credit Cards Still Win

Look, credit cards exist for a reason. There are cases where they are simply the better tool:

You sell directly to consumers: Whether it is in a physical store or online, most people reach for their card first. Making them go find their routing number is asking too much, and you will lose sales.

You rely on impulse or one-time purchases: The easier you make a checkout, the more you sell. Credit cards are built for exactly this kind of friction-free transaction.

You have international customers: ACH is mostly a domestic system.A credit card is typically the only realistic option if someone from a foreign country pays you.

Many consumers feel safer knowing they can dispute a charge if something goes wrong. Your customers care about buyer protection. Whether we like it or not, that peace of mind drives your purchasing decision.

What About Security? Which One Is Actually Safer?

Neither one is perfect, let’s be honest about that.

Unauthorized transactions are the primary risk of ACH. If anyone obtains a customer’s bank account details, that is a problem. That said, bank account numbers are not shared as casually as card numbers, so the exposure is generally lower.

With credit cards, chargebacks are the bigger headache. A customer can dispute a transaction weeks after it happened, the money gets pulled back from your account, and you are stuck proving the sale was legitimate. The chargeback process is slow, stressful, and sometimes unfair to merchants.

When comparing ACH vs Credit Card Payments purely on risk, most merchants will tell you chargebacks are the bigger day-to-day problem. ACH disputes happen, but they are far less common.

Thinking About Cash Flow: Which One Helps More?

This one matters a lot more than people give it credit for.

With ACH recurring billing, your cash flow becomes predictable. You know when money is coming in. You can plan around it. That stability is genuinely valuable when you are managing expenses, vendor payments, and payroll.

Credit cards introduce more uncertainty. Chargebacks can reverse payments long after the fact. Holds, reserves, and processing delays can throw off your timing in ways that ACH usually does not.

For businesses that live and breathe on steady cash flow; which is most of them; ACH offers a level of consistency that credit cards simply cannot match.

You Do Not Have to Pick Just One

Here is what actually works for most businesses: use both, but use them strategically.

- Credit cards for retail, e-commerce, one-time consumer purchases, and anything where checkout speed matters

- ACH for recurring billing, large invoices, B2B payments, and payroll

This is not a complicated strategy. It is just using the right tool for the right job. A lot of payment platforms today make it easy to offer both options without a ton of technical setup.

FAQs: ACH vs Credit Card Payments

Q: Is ACH cheaper than credit cards?

A: Yes, almost always. ACH uses flat fees while credit cards charge a percentage, which adds up fast on larger transactions.

Q: Which has more chargeback risk?

A: Credit cards carry significantly more chargeback risk than ACH payments.

Q: Is ACH safe for customers?

A: Yes. ACH is protected under federal banking regulations and is one of the most widely trusted payment systems in the country.

Q: Can I offer both ACH and credit card at checkout?

A: Yes, and many businesses do. Offering both gives customers flexibility and helps you manage costs.

Q: What types of businesses benefit most from ACH?

A: SaaS companies, law firms, insurance agencies, staffing firms, and any business with recurring billing or high-value invoices.

Q: Do credit cards or ACH settle faster?

A: Both are roughly similar; one to two days for credit cards, one to three for ACH; though same-day ACH has narrowed the gap.

The Bottom Line

There is no universal winner in the ACH vs Credit Card Payments debate. What there is, is a smarter way to think about it. Stop treating payment methods as a one-size-fits-all decision and start matching the method to the transaction.

High-value invoice going out to a business client? ACH. Retail customers checking out online? Credit card. Monthly subscription? ACH. International order? Credit card.

Once you start thinking this way, you will likely find that you save money, reduce disputes, and create a smoother experience for your customers at the same time. That is not a bad outcome for what is essentially just a billing decision. To explore payment tools that support this kind of flexibility, visit https://p2ezpay.com/